Social Science Money and Credit Important Questions

Very Short Answer Questions (VSA) 1 Mark

Question 1.

The currency notes on behalf of the Central Government are issued by whom?

Answer:

Reserve Bank of India.

Question 2.

Why do banks ask for collateral while giving credit to a borrower?

Answer:

Collateral is an asset that the borrower owns (land, building, vehicle,

livestock, land documents, deposits with banks, etc.) which stands as a security

against the money borrowed. In case the borrower fails to repay the loan, the

lender has the right to sell the asset or collateral.

Question 3.

What do banks do with the deposits they accept from customers?

Answer:

Banks use a major portion of deposits to extend loans to people.

Question 4.

What comprises ‘terms of credit’?

Answer:

Interest rate, collateral and documentation requirement and mode of repayment

together comprise terms of credit.

Question 5.

What is the main informal source of credit for rural households in India?

Answer:

Money lenders are the main source of informal credit for rural households.

Question 6.

Which body supervises the functioning of formal sources of loans?

Answer:

Reserve Bank of India.

Question 7.

‘Modern currency is without any use of its own’; then why is it accepted as a

medium of exchange?

Answer:

Modern currency is accepted as a medium of exchange because it is certified for

a particular denomination (?10, ?100, etc.) of the country by authorities set up

by the Central Government. It is issued by the Reserve Bank of India and it can

be used for buying any commodity which is on sale. It is authorized by the

government of the country.

Question 8.

What is the meaning of ‘barter system’?

Answer:

Barter system refers to the system of exchange of goods and services. It is the

system by which one commodity is exchanged for another without the use of money.

Before money was introduced, people practised barter system.

Example: A farmer could buy a dhoti from a weaver or a pair of shoes from a

cobbler in exchange of grains he produced.

Question 9.

What is the meaning of ‘investment’?

Answer:

Investment is buying of an asset in the form of a factory, a machine, land and

building, etc. (physical assets) or shares (monetary assets) for the purpose of

making or sharing profits of the enterprises concerned.

Common investments are—buying land, factories, machines for faster production,

buying small local companies to expand production, cheap labour, skilled

engineers, IT personnel, etc.

Question 10.

What is meant by double coincidence of wants?

Answer:

Double coincidence of wants means when both parties have agreed to sell and buy

each other’s commodities.

Question 11.

How does money act as a medium of exchange?

Answer:

Money acts as a medium of exchange as it acts as an intermediate in the exchange

process and transactions. A person holding money can easily exchange it for any

commodity or services that he or she might want.

Question 12.

How do the deposits with banks become their source of income?

Answer:

Banks charge a higher interest rate on loans they extend than what they offer on

deposits. The difference of interest is the main source of income of banks.

Question 13.

Why one cannot refuse a payment made in rupees in India?

Answer:

One cannot refuse a payment made in rupees in India because it is accepted as a

medium of exchange. The currency is authorized by the government of the country.

Question 14.

Compare formal sector loans with informal sector of loans regarding interest

only.

Answer:

Most of the informal lenders charge a much higher interest on loans than the

formal sector

Question 15.

Why is the supervision of the functioning of formal sources of loans necessary?

Answer:

Supervision of the functioning of formal sources of loans is necessary because

banks have to submit information to the RBI on how much they are lending, to

whom they are lending and at what interest rate etc.

Question 16.

Prove with an argument that there is a great need to expand formal sources of

credit in rural India.

Answer:

There is great need to expand formal sources of credit in rural India because:

1. There is

no organisation that supervises the credit activities of lenders in the informal

sector. They lend at whatever interest rate they choose.

2. No one

can stop rural money-lenders from using unfair means to get their money back.

Question 17.

Why are most of the poor households deprived from the formal sector of loans?

(2016 OD)

Answer:

Most of the poor households are deprived from the formal sector loans because of

lack of proper documents and absence of collateral.

Question 18.

What do you understand by demand deposits?

Answer:

To ensure safety of their money, people deposit their money with banks. Banks

accept deposits and pay interest on deposits. People have the provision to

withdraw their money as and when they require. Since money can be withdrawn on

demand, these deposits are known as demand deposits.

Features:

1. A demand

deposit has the essential characteristic of money. It can be used as a medium of

exchange.

2. The

facility of cheques against demand deposits makes it possible to make payments,

without using cash.

3. Since

demand deposits are accepted widely as a means of payment along with currency,

they constitute money in the modem economy.

Question 19.

Which country has successfully organized SHGs? Who had initiated the programme?

Answer:

Bangladesh has successfully organized SHGs. Grameen Bank of Bangladesh is the

biggest success story in reaching the poor to meet their credit needs at

reasonable rates. Grameen Bank has now over 6 million borrowers in 40,000

villages across Bangladesh. Most of the borrowers are women and belong to the

poorest section of society. This idea is the brain child of Prof. Mohammad

Yunus, recipient of 2006 Nobel Prize for Peace.

Question 20.

Highlight the inherent problem in double coincidence of wants.

Answer:

Double coincidence of wants means that when someone wants to exchange his goods

with another person, the latter must also be willing to exchange his goods with

the first person. It can only work when both the persons are ready to exchange

each other’s goods.

Question 21.

How does the use of money make it easier to exchange things? Give an example.

Answer:

The use of money solves the problem of double coincidence of wants. Money acts

as a medium of exchange and serves as a unit of value.

Question 22.

Who issues currency in India?

Answer:

The Reserve Bank of India issues currency in India.

Question 23.

Mention the form of modem currency

Answer:

Usually, there are two forms of modem currency. Those are (a) paper currency,

(b) coins.

Question 24.

What is Money Supply?

Answer:

Money supply refers to total money in circulation in any country at a given

point of time.

Question 25.

What is paper money? What is its use?

Answer:

Money made of paper is called paper money. It is easy to carry

Question 26.

What do you know about Muhammad Yunns?

Answer:

Muhammad Yunus founded the Grameen Bank in Bangladesh. He got Nobel Peace prize

in 2006.

Question 27.

What do you mean by a bank?

Answer:

A bank is an institution which deals with the transaction of money and credit.

Question 28.

What is a commercial bank?

Answer:

A commercial bank is a financial institution which deals with money and credit

with a view to earn profit.

Question 29.

What is credit control?

Answer:

Credit control is the regulation of credit by the RBI for achieving certain

objectives like price stability, growth and exchange rate stab ill ty.

Question 30.

Define moral suasion?

Answer:

Moral suasion means persuasion, request and appeal by the RBI to the

member-banks so to expand and control credit.

Question 31.

What eliminates the need for double coincidence wants?

Answer:

Money eliminates the double coincidence of wants.

Question 32.

What is called the medium of exchange?

Answer:

Money as an intermediate in the exchange process is rightly called the medium of

exchange.

Question 33.

How do we deposit money in the bank?

Answer:

We deposit money in the bank by opening an account. The money so deposited in

the bank is credited to our account.

Question 34.

What will happen if all the depositors ask for their money from the bank?

Answer:

The bank will have to seek deposits from other sources or will have to ask its

borrowers to give back the money.

Question 35.

Explain the meaning of the collateral?

Answer:

Collateral is an asset the borrower owns (such as to land, livestock, building

etc.) and uses this as a guarantee a lender until the loan is paid.

Question 36.

What do you mean by terms of credit?

Answer:

Interest rate, collateral and documentation requirements, and the mode of

repayment etc. comprise what is called the terms of Credit.

Question 37.

Explain how money acts as a medium of exchange?

Answer:

Money has a significant role in helping exchange or commodities. We sell our

products in return to get money. We buy products by giving money for the

products we want. Money acts as the intermediate, and thus eliminates the need

of the double coincidence of wants.

Question 38.

Why rupee is used, in India, as a medium of exchange?

Answer:

As per law, it is only the Reserve Bank of India which issues paper notes. We

find rupee as a paper note. No individual has been authorised to issue rupees in

the form of paper currency Law recognises the use of rupees as a medium of

making payment. It is used in settling transactions in India. No individual in

India can legally refuse a payment made in rupees.

Question 39.

Why do the cheques constitute money- in the modem currency?

Answer:

We buy products by making payment through cash.

Question 40.

Give briefly the functions of money.

Answer:

Money, in the form of cash or cheques, is a medium of exchange. Its functions,

briefly, are:

1. it acts

as a medium of exchange,

2. it acts

as a measure of value;

3. it is

source of store of value;

4. it helps

us transfer value;

5. it acts

as a standard for deferred payments.

Question 41.

Differentiate between demand deposits and fixed deposits

Answer:

Demand deposits can be written down from the bank without any notice; fixed

deposits are withdrawn only at the time of maturity. Demand deposits are

chequable; fixed deposits are not chequable. Demand deposit constitute a part of

money supply while the fixed deposits come under the category of near money.

Question 42.

Why are demand deposits considered as money?

Answer:

M.Salim will write a cheque in the name of a person from whom he buys on a

products. Then he will write the specific amount both in words and figures. On

the right top of the cheque, he will specify the date, and down below in the

right, he will sign the cheque.

Salim’s balance in his bank account decreases and Prem’s balance

increases.

As the deposits in the bank can be withdrawn on demand, they act as money.

One can issue a cheque and ask for money against one’s deposits in the bank. If

you do not have deposits in the bank, you cannot withdraw money. Supposing,

Salim continues to get orders from traders. What would be his position after 6

years.

Question 43.

What are the reasons that make Swapna’s situation so risky? Discuss the

following factors pesticides role of moneylenders; climate.

Answer:

1. Salim is

a small trader. He wants to buy stock so to sell it at the time of festival in

the following month.

2. The risk

is that if he does not get credit, he would not able to buy stock and shall not

earn profit.

3. Salim was

able to obtain credit from the bank against some security. He got the loan, had

bought the stocks and earning profit when he sold the stock.

Salim would be able to make profit year after year his business will

expand.

Swapna took loan from the moneylender and paid a higher rate of interest.

But what she bought for her farming expenses, she did not obtain the desired

result. Unfortunately, her crop failed. She was caught up in debit. She had to

pay to the moneylender a high amount in the form of interesct.

Question 44.

Why should the people deposit money with bank

Answer:

People hold money as deposit with the bank. At a point of time, people need only

some currency for their day-to-day needs. For instance, workers who receive

their salaries at the end of each month have extra cash at the beginning of the

month.

They deposit it with the banks by opening a bank account in their name.

Banks accept the deposits and also pay an interest rate on the deposits. In this

way people’s money is safe with the banks and it earns an interest. People also

have the provision to withdraw the money as and when they require. Since the

deposits in the bank accounts can be withdrawn on demand, these deposits are

called demand deposits.

Demand deposits offer another interesting facility. It is this facility

which lends it the essential characteristics of money (that of a medium of

exchange). One would like to make payments by cheques instead of cash. For

payment through cheque, the payer who has an account with the bank makes out a

cheque for a specific amount. A cheque is a paper instructing the bank to pay a

specific amount from the person’s account to the person in whose name the cheque

has been made.

Question 45.

What does the bank do with the deposits it has?

Answer:

Banks has the deposits from the people. It keeps only a small proportion of

their deposits as cash with themselves. For example, banks in India these days

hold about 15 per cent of their deposits as cash. This is kept as provision to

pay the depositors who might come to withdraw money from the bank on any day.

Since, on any particular day, only some of its many depositors come to withdraw

cash, the bank is able to manage with this cash.

Banks use the major portion of the deposits to extend loans. There is a

huge demand for loans for various economic activities banks make use of the

deposits to meet the loan requirement of the people. In this way, banks mediate

between those who a surplus funds (the depositors) and those who are in need

these funds (the borrowers). Banks charge a higher interest rate on loans than

what they offer on deposits. The difference between what is charge from

borrowers and what is paid to depositors is their main source of income.

Question 46.

What do you mean by terms of credit? Why do the lender aks for collateral

against loan?

Answer:

Interest rate, collateral and documentation requirements, and the mode of

repayment together comprise what is called the terms of credit. The terms of

credit vary substantially from one another. Every loan agreement specific an

interest which the borrower must pay me lender along with the repayment of the

principal.

In addition, lenders may demand collateral (i.e. security against loan).

Collateral is an asset that the borrower own, such as land, building, vehicle,

livestock, deposits with the bank and uses this as guarantee to a lender until

the loan is refunded. If the borrower fails to repay the loan, the lender has

the right to sell the asset or collateral to obtain repayment payment such as

land titles, deposits with banks livestock are some common examples of

collateral used for borrowing.

Question 47.

What are formal and informal sector loans? Who supervises the functioning of

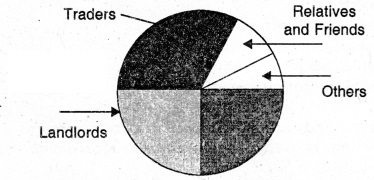

formal sources of loans and how?

Answer:

Various types of loans can be grouped as formal sector loans and informal sector

loans. Banks and cooperatives are examples of formal sector loans whereas

informal sector loans include loans from money lenders, traders, employers,

relatives and friends. The chart here refers to sources of credit for Rural

Households in India in 2003.

Sources of Credit for Rural Households in India in 2003.

The Reserve Bank of India supervises the functioning of formal sources of

loans. For instance, the banks maintain a minimum cash balance out of the

deposits they receive. The RBI monitor that the banks actually maintain the cash

balance. Similarly, the RBI sees that the banks give loans not just to

profit-make into business and traders but also to small cultivators, small scale

industries, to small borrowers etc. Periodically, banks have to submit

information to the RBI on how much they are lending to whom, at what interest

rate, etc.

Question 48.

Write a note on ‘Self Help Group’.

Answer:

In recent years, people have tried out some newer ways of providing loans to the

poor. The idea is to organise rural poor, in particular women, into small Self

Help Groups (SHGs) and pool (collect) their savings. A typical SHG has 15-20

members, usually belonging to one neighbourhood, who meet and save Regularly.

Saving per member varies from ₹ 25 to ₹ 100 or more, depending on the ability of

the people to save.

Members can take small loans from the group itself to meet their needs.

The group charges interest on these loans but this is still less than what the

moneylender charges. After a year or two, if the group is regular in savings, it

becomes eligible for availing loan from the bank.

The SHGs help borrowers overcome the problem of lack of collateral. They

can get timely loans for a variety of purposes and at a reasonable interest

rate. Moreover, SHGs are the building blocks of organisation of the rural poor.

Not only does it help women to become financially self-reliant, but the regular

meetings of the group also provide a platform to discuss and act on a variety of

social issues such as health, nutrition, domestic violence, etc.

Short Answer Questions (SA) 3 Marks

Question 49.

What is money? Why is modern money currency accepted as a medium of exchange?

Answer:

Money is a medium of exchange in transactions. A person holding money can easily

exchange it for any commodity or service that he or she might want.

Modem money currency is accepted as a medium of exchange because

1. it is

certified for a particular denomination (For example, ₹ 10, ₹ 20, ₹ 100, ₹

1,000).

2. it is

issued by the Central Bank of the country.

3. it is

authorized by the government of the country.

Question 50.

What are the modern forms of money? Why the ‘rupee’ is widely accepted as a

medium of exchange? Explain two reasons.

Or

Why is modern currency accepted as a medium of exchange without any use of its

own? Give reasons?

Answer:

Modem forms of money currency in India include paper notes and coins which are

known as Rupees and Paisa.

1. It is

accepted as a medium of exchange because the currency is authorized by the

Government of India.

2. In India,

the Reserve bank of India issues currency notes on behalf of the Central

Government of India.

3. The law

legalizes the use of rupee as a medium of payment that cannot be refused in

settling transaction in India.

4. No

Individual in India can legally refuse a payment made in rupees.

Therefore, the rupee is widely accepted as a medium of exchange.

Question 51.

What is collateral? Why do lenders ask for collateral while lending? Explain.

Answer:

Collateral is an asset that the borrower owns (land, building, vehicle,

livestock, land documents, deposits with banks etc.) which stands as a security

against the money borrowed. In case the borrower fails to repay the loan, the

lender has the right to sell the asset or collateral to recover the loan money.

Most lenders ask for collateral while lending as a security against their own

funds.

Question 52.

“Cheap and affordable credit is essential for poor households both in rural and

urban areas.” In the light of the above statement explain the social and

economic values attached to it.

Or

“Cheap and affordable credit is crucial for the country’s development.” Assess

the statement.

Or

‘Credit has its own unique role for development’. Justify the statement with

arguments.

Answer:

Credit means loAnswer: It refers to an agreement in which the lender supplies

the borrower with money, goods or services in return for the promise of future

repayment.

1. Cheap and

affordable credit is crucial for the country’s growth and economic development.

Credit is in great demand for various kinds of economic activities—big or small

investments, to set up business, buying cars, houses, etc.

2. In rural

areas credit helps in the development of agriculture by providing funds to

farmers to buy seeds, fertilizers, expensive pesticides.

3.

Manufacturers need credit for buying raw material or to meet ongoing expenditure

of production. Credit helps in the purchase of plant, machinery, equipment, etc.

4. Some

people may need to borrow for illness, marriages etc.

Thus, cheap and affordable credit is crucial for the country’s growth and

economic development.

Question 53.

How does money solve the problem of double coincidence of wants? Explain with an

example.

Answer:

Money acts as a medium of exchange. Money can be exchanged for any kind of

commodity or service of one’s choice or need. Before money was introduced,

people practised barter system. They exchanged goods with each other.

Example, A farmer could buy a dhoti from a weaver or a pair of shoes from a

cobbler in exchange of grains he produced.

The problem with the barter system was that both the parties had to agree

to sell and buy each other’s product. This is known as double coincidence of

wants.

In barter system, where goods are directly exchanged without the use of

money, it is essential that there is a double coincidence. Double coincidence is

a situation where two persons need or desire to have each other’s product.

Money solves this problem as with money we can buy whatever we want and

whenever we want, without having to exchange something in return.

Question 54.

How is money used in everyday life? Explain with examples.

Answer:

1. Money

plays a central role in our daily life. It is used as a medium of exchange to

carry out transactions.

2. Money

buys us food, clothing, shelter and other basic necessities of life.

3. Money

provides us social security. It is needed to procure services like transport,

education, healthcare, entertainment, recreation, and so on. Money facilitates

business and trade and is the basis of the working of an economy.

Question 55.

Explain with examples, how people are involved with the banks.

Answer:

1. Banks

help people to save their money and keep their money in safe custody of the

bank. Banks accept deposits from the public and also help people to earn

interest on their deposits.

2. People

can withdraw the money deposited with the bank at the time of their need. As the

money can be withdrawn on demand, these are called demand deposits.

3. Banks

also grant loans to people for a variety of purposes. In times of need

individuals, business houses and industries can borrow money from the banks.

Question 56.

Why is it necessary for the banks and cooperative societies to increase their

lending facilities in rural areas? Explain.

Answer:

Banks and Cooperatives can help people in obtaining cheap and affordable loans.

This will help people to grow crops, do business, set up small-scale industries

or trade in goods and also help indirectly in the country’s development. They

should do so, so that relatively poor people do not have to depend on informal

sources of credit (money-lenders).

Question 57.

How can money be easily exchanged for goods or services? Give an example to

explain.

Answer:

Money as a medium of exchange for goods and services:

A person holding money can easily exchange it for any commodity or service that

he or she might want. Everyone prefers to receive payments in money and exchange

the money for things they want.

For example: A shoemaker wants to sell shoes in the market and buy wheat.

The shoe maker will first exchange shoes for money and then exchange the money

for wheat. If the shoemaker had to directly exchange shoes for wheat without the

use of money, he would have to look for a wheat growing farmer who not only

wants to sell wheat but also wants to buy the shoes in exchange. Both the

parties have to agree to sell and buy each other’s commodities. This process is

very difficult, time consuming and unhealthy.

Question 58.

“The credit activities of the informal sector should be discouraged.” Support

the statement with arguments.

Answer:

The credit activities of the informal sector should be discouraged because:

1. 85% of

loans taken by the poor households in the urban areas are from informal sources.

There is no organisation that supervises the credit activities of lenders in the

informal sector.

2. Informal

lenders charge very high interest on their loAnswer: They try to charge more and

more interest on their loans as there are no boundaries and restrictions.

3. Higher

cost of borrowing means a larger part of the earnings of the borrowers is used

to repay the loan.

4. In

certain cases, the high interest rate for borrowing can mean that the amount to

be repaid is greater than the income of borrower. This could lead to increasing

debt and debt trap, therefore the credit activities of the informal sector

should be discouraged.

Question 59.

Why do we need to expand formal sources of credit in India?

Answer:

1. There is

no organisation that supervises the credit activities of lenders in the informal

sector. They lend at whatever interest rate they choose.

2. No one

can stop rural money-lenders from using unfair means to get their money back.

3. Informal

lenders charge a very high rate of interest on loans and as a result a larger

part of the earnings of the borrowers and farmers are used to pay the loans.

4. The

amount to be repaid is often greater than income, and farmers and other

borrowers in villages fall in a debt trap.

Thus, it is necessary that banks and co-operatives increase their lending,

particularly in rural areas, so that dependence on informal sources of credit

ends.

Long Answer Questions (LA) 5 Marks

Question 60.

What is the basic objective of ‘Self Help Groups’? How do they work? Describe

any four advantages of ‘Self Help Groups’ for the poor.

Answer:

The basic objective of ‘Self Help Groups’ is to organize rural poor,

particularly women belonging to one neighbourhood into small Self Help Groups

(15-20 members). These members save regularly and the amount varies from ₹25-100

or more depending upon their ability to save.

The four advantages of ‘Self Help Groups’ are as follows:

1. The

members can take small loans from the group itself to meet their needs. The

group charges interest on these loans which is still less than what moneylenders

charge.

2. After a

year or two, if the group is regular in savings, it becomes eligible for

availing loan from the bank which is sanctioned in the name of the group to

create self-employment opportunities. All important decisions regarding loan,

purpose, amount of interest, non-payment of loan are taken by the group members.

For instance, small loans are provided to the members for releasing mortgaged

land, meeting working capital needs, for acquiring assets like sewing machines,

handlooms, cattle etc.

3. Since

non-repayment of loans is dealt with seriously by group members, therefore banks

are willing to lend to the poor women when organized in SHGs, even though they

have no collateral as such. Thus, the SHGs help women to become financially

self-reliant.

4. The

regular meetings of the group provide a platform to discuss and act on a variety

of social issues such as health, nutrition, domestic violence etc.

Question 61.

‘Banks and cooperatives help people in obtaining cheap and affordable loans’

which values according to you does this support?

Answer:

Cheap and affordable loans help people to grow crops, do business, set up small

scale industries or trade in goods.

This promotes:

1.

Self-reliance and financial security and independence of people.

2.

Protection of the relatively poor against corrupt moneylenders.

3.

Eradication of poverty in general.

4. All this

indirectly helps in the country’s development.

Question 62.

What is Credit? Why is cheap and affordable credit important for the country’s

development? Give four reasons.

Or

What is credit? Explain with an example, how credit plays a vital and positive

role for development.

Answer:

Credit means loans. It refers to an agreement in which the lender supplies the

borrower with money, goods or services in return for the promise of future

repayment.

1. Cheap and

affordable credit is crucial for the country’s growth and economic development.

Credit is in great demand for various kinds of economic activities—big or small

investments, to set up business, buying cars, houses, etc.

2. In rural

areas credit helps in the development of agriculture by providing funds to

farmers to buy seeds, fertilizers, expensive pesticides.

3.

Manufacturers need credit for buying raw material or to meet ongoing expenditure

of production. Credit helps in the purchase of plant, machinery, equipment, etc.

4. Some

people may need to borrow for illness, marriages etc.

Thus, cheap and affordable credit is crucial for the country’s growth and

economic development.

Question 63.

What are the two categories of sources of credit? Mention four features of each.

Answer:

The two sources of credit are formal sources and informal sources:

Formal sources of credit:

1. Banks and

cooperative societies fall under the formal sector. One can obtain loans from

banks or cooperative societies.

2. The

Reserve Bank of India supervises the functioning of formal sources of loAnswer:

3. Bank

loans require documentation and collateral (collateral is an asset such as land,

building, vehicle, livestock, deposits with the bank, etc.). This is used as a

guarantee to the lender until the loan is paid back.

4. Formal

sources cannot charge any rate of interest from the borrowers according to their

whims.

Informal sources of credit:

1. In the

informal sector money can be borrowed from a person, friend, relative,

moneylender, traders, employers, etc.

2. There is

no organization that checks or supervises the activities of lenders in the

informal sector.

3. Loans

from informal sources do not require any such collateral.

4. They

charge a very high rate of interest on loans as they do not require any

collateral.

Question 64.

Which government body supervises the functioning of formal sources of loans in

India? Explain its functioning.

Answer:

The Reserve Bank of India supervises the functioning of formal sources of loans.

Functions of Reserve Bank of India.

1. RBI

requires commercial banks to maintain a minimum cash balance out of the deposits

they receive. The RBI monitors that the banks actually maintain the cash

balance.

2. RBI sees

that the banks give loans not just to profit-making businesses and traders but

also to small cultivators, small-scale industries, small borrowers, SHGs, etc.

3. RBI

issues guidelines for fixing rate of interest on deposits and lending by

commercial banks.

4.

Periodically, banks have to submit information to the RBI on how much they are

lending, to whom, at what interest rate, etc.

Question 65.

What are the various sources of credit in rural areas? Which one of them is the

most dominant source of credit and why?

Answer:

Moneylenders are the most dominant amongst sources of credit for rural

households. They constitute an informal source of credit. They charge a very

high rate of interest on loans as they do not require any collateral. They are

the most convenient source of credit in the rural areas.

Other sources of rural credit:

1.

Cooperative Societies are another major source of rural credit. They are a

source of formal sector credit. Members of a Cooperative pool their resources

for helping one another, e.g., Farmers’ Cooperatives, Weavers’ Cooperatives,

etc. They offer cheap credit in rural areas for their members. Once these loans

are repaid, another round of loans is offered.

2.

Agricultural traders, relatives and friends are other informal sources of rural

credit. Some farmers borrow from agricultural traders who supply the farm inputs

(such as seeds, fertilizers, pesticides, etc.) on credit at the beginning of the

cropping season and repay the loans after the harvest.

3.

Commercial banks also give loans to rural households. However, not many rural

households borrow from banks as they require proper documentation and

collateral.

Question 66.

“Deposits with the banks are beneficial to the depositors as well as to the

nation”. Examine the statement.

Answer:

Benefit of deposits to the depositors:

1. Bank

accepts the deposits and pays interest to the depositor.

2. Banks

help people save their money and keep their money in safe custody of the bank.

3. People

can withdraw the money as and when they require.

4. Banks

also grant loans to people for a variety of purposes. In times of need,

individuals, business houses and industries can borrow money from the banks.

Benefit of deposits to the Nation:

1. Banks use

the major proportion of the deposit to extend loans.

2. There is

a huge demand for loans for various economic activities. In times of need,

business houses and industries can borrow money from the banks.

3. Banks

mediate between those who have surplus funds and those who are in need of these

funds. Thus, it helps in the economic development of the Nation.

Question 67.

How do banks play an important role in the economy of India? Explain.

Answer:

1. Banks

help people to save their money and keep their money in safe custody. To ensure

safety of their money, people deposit their money with banks. Banks accept

deposits and pay interest on deposits. People have the provision to withdraw

their money as and when they require.

2. Banks

also grant loans to people for a variety of purposes. In times of need

individuals, business houses and industries can borrow money from the banks.

3. Credit

provided by banks is crucial for the country’s growth and economic development.

Credit is needed for all kinds of economic activities, to set up business, buy

cars, houses, etc.

4. Banks

also help people in obtaining cheap and affordable loans. This can help people

to grow crops, do business, set up small-scale industries or trade in goods and

also help indirectly in the country’s development. They should do so, so that

relatively poor people do not have to depend on informal sources of credit

(money-lenders).

Question 68.

Describe the vital and positive role of credit with examples.

Answer:

In the festive season, a shoe manufacturer, Ram receives an order from a large

trader in town for 3,000 pairs of shoes to be delivered in a month’s time. To

complete production on time Ram has to hire workers for stitching and pasting

work. He has to purchase the raw materials. To meet these expenses Ram obtains

loans from two sources.

First, he asks the leather supplier to supply leather now and promises to

pay him later.

Second, he obtains loan in cash from the large traders as advance payment

for 1000 pairs of shoes with a promise to deliver the whole order by the end of

the month.

At the end of the month, Salim is able to deliver the order, make a good

profit and repay the money he had borrowed.

Salim obtains credit to meet the working capital needs of production. The

credit helps him to meet the ongoing expenses of production, complete production

on time and thus increase his earnings. Credit therefore plays a vital and

positive role in this situation.

Question 69.

How can the formal sector loans be made beneficial for poor farmers and workers?

Suggest any five measures.

Answer:

Formal sector loans can be made beneficial for poor farmers and workers in the

following ways:

1. Create

greater awareness among farmers about formal sector loans.

2. Process

of providing loans should be made easier. It should be simple, fast and timely.

3. More

number of Nationalized Banks/cooperative banks should be opened in rural

sectors. Banks and cooperatives should increase facility of providing loans so

that dependence on informal sources of credit reduces.

4. The

benefits of loans should be extended to poor farmers and small scale industries.

5. While

formal sector loans need to expand, it is also necessary that everyone receives

these loans. It is important that formal credit is distributed more equally so

that the poor can benefit from cheaper loans